Condensate Pricing Premium

Whilst looking into infrastructure development in Western Canada, I saw that Keyera recently announced the completion of their Key Access Pipeline System (KAPS). Pembina has also been expanding with similar infrastructure investments.

So why invest in this infrastructure?

- Pembina is currently constructing their Phase VIII Pipeline expansion. With an estimated $530 million project cost, this expansion will provide separate pipelines for ethane-plus and propane-plus NGL mix from Gordondale, Alberta to the Edmonton. This project involves constructing approximately 150 kms of both 10” and 16” pipeline, additional mid-point pump capacity, and terminal upgrades.

- Infrastructure such as this facilitates the recovery and separation (e.g., fractionation) of natural gas liquids (NGLs) from natural gas. This has many benefits including the production of condensate.

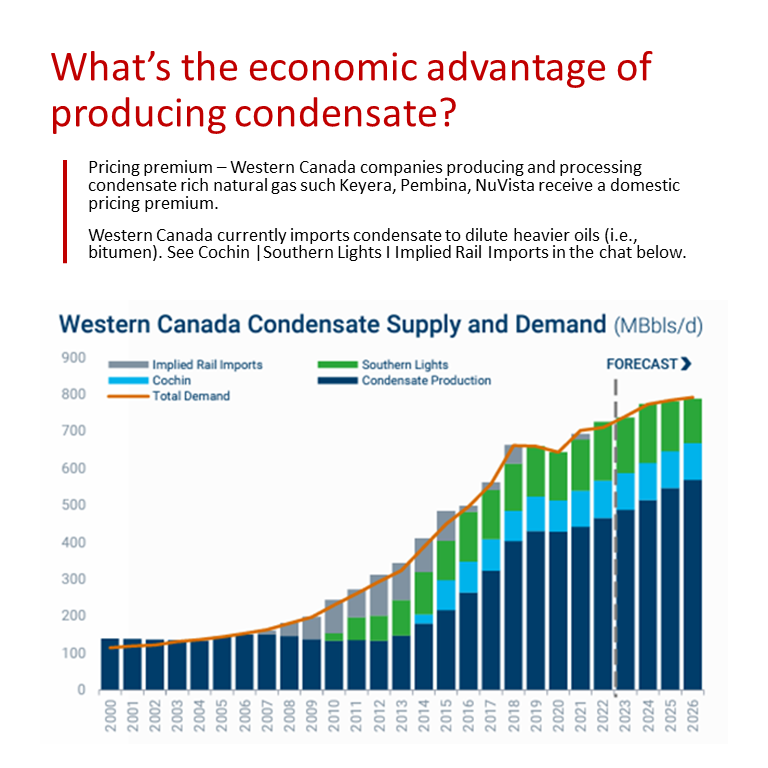

- Condensate is commonly sold as dilute for the dilution of heavy oils (i.e., bitumen) produced in the Western Canadian region. Dilute reduces the density and viscosity of these heavier oils.

- Domestic demand of dilute (e.g., condensate) far exceeds supply. As result, dilute is imported at a pricing premium.

- Local companies involved in the production and processing of natural gas liquids such Keyera, Pembina, NuVista, and others receive this pricing premium.

- In contrast, many of Western Canada’s oil and gas resources are sold at a discount (e.g., differential). This is a result of several factors including basic supply and demand dynamics.

Interested in working together?

It starts with a conversation – send me LinkedIn message or email (Jamie.Clarke@jwcsolutions.ca). Let’s start with the 30,000-foot view and refine the details as we go. If I can’t help, I may know someone who can.

#canadianenergy #energy #oilandgas #engineering #Keyera #NuVista #Pembina